New car registrations: +4.3% in June 2024; battery electric 14.4% market share

2024-07-18

Navigating the Shifting Landscape of European Car Sales

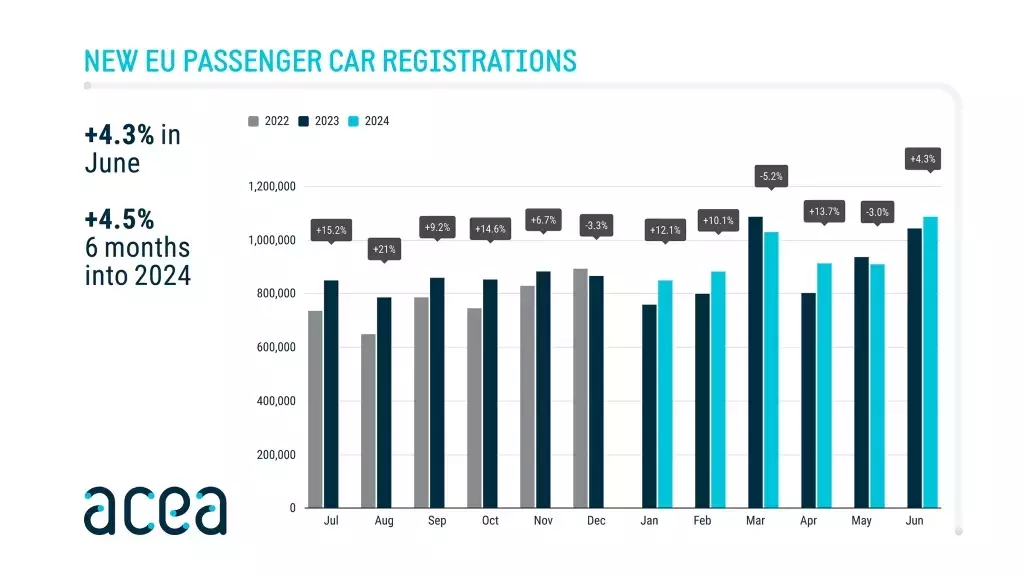

The European automobile industry has faced a rollercoaster of challenges in recent years, but the latest data suggests a glimmer of hope. In June 2024, EU car registrations saw a 4.3% increase, driven by gains in key markets like Italy, Germany, and Spain. However, the recovery remains fragile, with registration volumes still lagging behind pre-pandemic levels. As the industry navigates this evolving landscape, stakeholders must adapt to shifting consumer preferences and regulatory changes to secure a sustainable future.

Powering the Future: Trends in Alternative Fuel Vehicles

The Rise of Hybrid-Electric Vehicles

The European car market is undergoing a significant transformation, with hybrid-electric vehicles (HEVs) emerging as a dominant force. In June 2024, HEV registrations surged by 26.4%, with double-digit gains across the major markets of France, Italy, Spain, and Germany. This growth has propelled HEVs to a 29.5% market share, up from 24.4% the previous year. The appeal of HEVs lies in their ability to offer a balance between environmental consciousness and practical driving range, making them an increasingly attractive option for consumers.

The Ebb and Flow of Battery-Electric Vehicles

While battery-electric vehicles (BEVs) have been the darlings of the industry, their market share dipped slightly in June 2024, accounting for 14.4% of the EU car market, down from 15.1% the previous year. This decline can be attributed to double-digit drops in key markets like Germany, the Netherlands, and France, offsetting gains in Belgium and Italy. Despite the temporary setback, the long-term trajectory for BEVs remains positive, with a total of 712,637 new registrations in the first half of 2024, marking a modest 1.3% increase from the same period the previous year.

The Waning Popularity of Plug-in Hybrids

In contrast to the rising fortunes of HEVs, the plug-in hybrid electric vehicle (PHEV) segment experienced a significant decline of 19.9% in June 2024. This downturn was particularly pronounced in Belgium, France, and Germany, the largest markets for PHEVs. As a result, PHEVs now account for only 6.1% of the total car market, down from 7.9% the previous year. The shift away from PHEVs reflects the growing consumer preference for either pure electric or traditional hybrid solutions, leaving the PHEV segment in a precarious position.

The Enduring Presence of Petrol and Diesel

Despite the industry's push towards electrification, petrol and diesel-powered cars continue to maintain a significant presence in the European market. In June 2024, petrol car sales remained relatively stable, with a slight decline of 0.7%. Diesel cars saw a similar trend, with a slight drop of 0.9%. While the combined market share of petrol and diesel cars has fallen to 47.1%, down from 49.6% the previous year, these traditional powertrains still account for a substantial portion of the market, underscoring the need for a balanced approach to the energy transition.

Regional Variations and the Uneven Recovery

The recovery in the European car market has been uneven, with significant variations across the region's major markets. Italy, Germany, and Spain all experienced gains in June 2024, with increases of 15.1%, 6.1%, and 2.2%, respectively. In contrast, France saw a decline of 4.8% during the same period. This disparity is also reflected in the first half of 2024, where Spain (+5.9%), Germany (+5.4%), and Italy (+5.4%) all recorded positive growth, while France lagged behind with a more modest increase of 2.8%. These regional differences highlight the need for tailored strategies and policies to support the industry's recovery across the EU.

The Road Ahead: Navigating Challenges and Opportunities

As the European automobile industry navigates this evolving landscape, stakeholders must adapt to a range of challenges and opportunities. The shift towards alternative fuel vehicles, the uneven recovery across markets, and the persistent presence of traditional powertrains all require a nuanced and strategic approach. Manufacturers, policymakers, and consumers must work together to shape a sustainable future for the industry, one that balances environmental concerns, consumer preferences, and economic realities. By embracing innovation, fostering collaboration, and prioritizing adaptability, the European car market can emerge stronger and more resilient, poised to lead the way in the global automotive landscape.